What Happens If Your Business Fails a Tax Audit? Legal and Financial Consequences

Failing a tax audit in the UAE can have severe implications for your business, including hefty penalties, legal challenges, and long-lasting reputational damage. Tax audits are designed to verify the accuracy of your financial statements and tax filings, ensuring that your business complies with local tax laws and regulations. When discrepancies arise and a business fails to meet these standards, the consequences can be significant. In this blog, we explore the potential legal and financial repercussions of failing a tax audit and provide practical strategies to help you take corrective measures and avoid costly fines.

Understanding the Importance of Tax Audits

Tax audits serve as a critical checkpoint for ensuring that businesses accurately report their income, expenses, and tax liabilities. The Federal Tax Authority (FTA) in the UAE conducts these audits to maintain financial transparency and protect public revenue. For businesses, a successful audit is not just about regulatory compliance—it builds trust with investors, creditors, and other stakeholders. Conversely, failing a tax audit can signal underlying issues within your financial systems and lead to serious consequences.

Key Objectives of a Tax Audit

Ensuring Compliance:

Tax audits confirm that your business complies with VAT, corporate tax (where applicable), and other regulatory requirements.

Detecting Errors and Fraud:

Audits help identify errors, discrepancies, or intentional misstatements in your financial records. Early detection is essential to correct issues before they escalate.

Promoting Transparency:

A clean audit report enhances your company’s credibility by demonstrating a commitment to honest and accurate financial reporting.

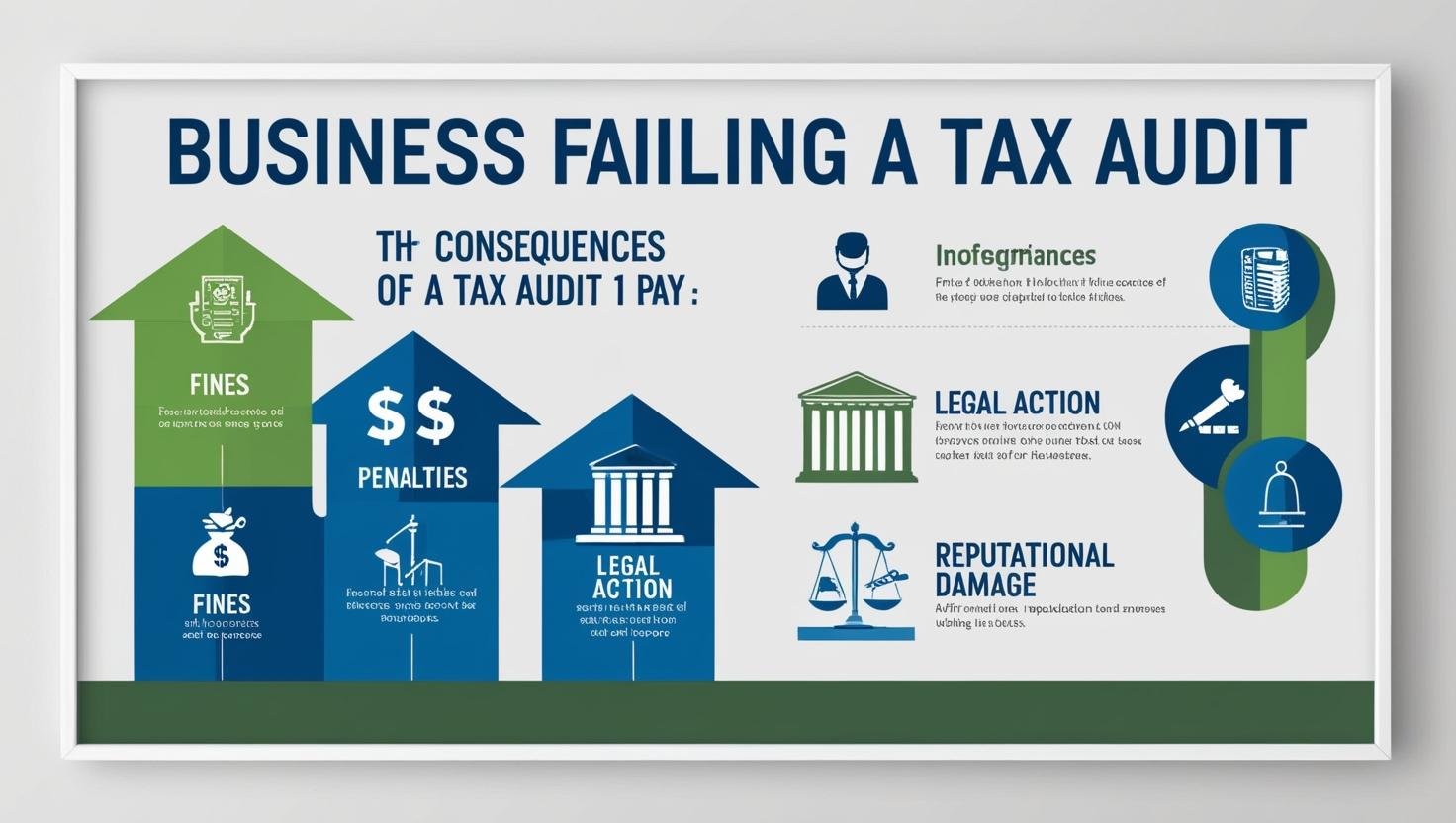

Legal Consequences of Failing a Tax Audit

When your business fails a tax audit, you may face a range of legal consequences that can disrupt operations and damage your company’s reputation.

1. Hefty Fines and Penalties

Monetary Penalties:

The FTA imposes substantial fines on businesses that do not comply with tax laws. These fines can be significant, depending on the severity and frequency of the discrepancies found during the audit.

Interest Charges:

In addition to fines, your business may be liable for interest on any underpaid taxes. This can substantially increase the financial burden on your company.

2. Legal Action and Litigation

Enforcement Proceedings:

If your business repeatedly fails to meet tax obligations, the FTA may initiate legal proceedings. This can result in court cases that are not only costly but also time-consuming.

License Suspension or Revocation:

In severe cases, regulatory authorities may suspend or revoke your business license. This can effectively force your company to cease operations, resulting in further financial losses and reputational harm.

3. Criminal Charges

Fraudulent Behavior:

If the audit reveals intentional manipulation or fraud—such as deliberately underreporting income or inflating deductions—business owners and key personnel may face criminal charges. Convictions in such cases can lead to imprisonment and permanent damage to personal and professional reputations.

Financial Consequences of Failing a Tax Audit

Beyond legal penalties, the financial implications of failing a tax audit can be crippling and may affect various aspects of your business.

1. Increased Tax Liabilities

Reassessment of Tax Obligations:

The FTA may reassess your tax liabilities based on the discrepancies found during the audit. This can lead to an increased tax bill, which might be significantly higher than the amount originally paid.

Retroactive Payments:

In some cases, businesses may be required to pay back taxes for previous periods, along with penalties and interest. This retroactive adjustment can strain your company’s cash flow.

2. Damage to Financial Reputation

Investor and Creditor Confidence:

A failed tax audit undermines the trust of investors, creditors, and financial institutions. This can result in difficulties securing future funding or obtaining favorable loan terms.

Market Perception:

News of non-compliance and financial discrepancies can spread quickly, tarnishing your brand and affecting your market position. Rebuilding trust after a failed audit can be a lengthy and costly process.

3. Operational Disruptions

Resource Diversion:

Dealing with the fallout from a failed tax audit can divert resources away from your core business operations. Time and money spent on legal proceedings, penalty settlements, and corrective measures can hinder growth and operational efficiency.

Increased Compliance Costs:

The need to overhaul internal controls, invest in new accounting systems, and engage external consultants to rectify the issues identified during the audit can lead to increased operational costs.

Corrective Measures to Avoid Failing a Tax Audit

Proactive planning and robust internal controls are essential for avoiding the pitfalls of a tax audit. Here are some strategies to help your business prepare effectively and minimize the risk of audit failure:

1. Maintain Robust Record-Keeping

Implement Modern Accounting Software:

Utilize advanced, cloud-based accounting systems to automate record-keeping and reconciliation processes. This minimizes human error and ensures that your financial data is up-to-date and accurate.

Standardize Documentation Procedures:

Establish clear, organization-wide policies for document retention and filing. This includes maintaining digital copies of invoices, receipts, bank statements, and tax returns, which are crucial during an audit.

2. Enhance Internal Controls

Segregation of Duties:

Divide responsibilities among different employees to reduce the risk of errors and fraud. Having separate teams for recording transactions, reconciling accounts, and approving payments can significantly improve accuracy.

Regular Internal Audits:

Conduct frequent internal audits to identify discrepancies early. This proactive approach allows you to address issues before they escalate to the level that would trigger an FTA audit.

Employee Training:

Provide regular training sessions for your finance and accounting teams to ensure they are well-versed in current tax laws, compliance requirements, and best practices for financial reporting.

3. Prepare Thoroughly for the Audit

Audit Readiness Checklist:

Develop a comprehensive checklist of all required documents and processes that need to be reviewed before an FTA audit. Regularly update this checklist and conduct pre-audit assessments to identify and rectify any deficiencies.

Designate an Audit Coordinator:

Appoint a dedicated point of contact to manage the audit process. This person should be responsible for gathering documents, liaising with auditors, and ensuring that any queries are addressed promptly.

Engage Professional Advisors:

Work with experienced tax advisors or audit firms that specialize in UAE tax audits. Their expertise can help you identify potential risks and implement corrective measures well in advance of an audit.

4. Foster a Culture of Transparency and Communication

Open Dialogue with Auditors:

Maintain clear and honest communication with auditors throughout the process. If discrepancies are identified, address them promptly and provide comprehensive explanations and supporting documents.

Regular Updates to Management:

Keep your leadership informed about audit preparations and any potential issues. This transparency ensures that corrective actions are implemented swiftly and effectively.

Continuous Improvement:

Use audit findings as an opportunity to refine your internal processes. Regularly review and update your financial management practices to adapt to evolving regulatory requirements and industry standards.

How Young and Right Can Help

Navigating the complexities of a tax audit can be challenging, but partnering with experienced professionals can transform the process from a daunting regulatory exercise into a strategic advantage. At Young and Right, we offer comprehensive tax audit services designed to help your business maintain compliance, optimize financial processes, and avoid costly penalties. Here’s how we support you:

1. Expert Analysis and Proactive Risk Management

In-Depth Regulatory Knowledge:

Our team stays current on the latest UAE tax laws and FTA regulations, ensuring that your financial records meet all legal requirements.

Advanced Fraud Detection:

We employ cutting-edge analytical tools to identify discrepancies and potential fraud early, allowing you to address issues proactively.

Detailed Financial Reviews:

Our comprehensive analysis uncovers misstatements and inefficiencies, providing you with a clear understanding of your financial position.

2. Tailored Audit Preparation Strategies

Customized Solutions:

We develop audit strategies tailored specifically to your business’s unique needs, ensuring that every aspect of your financial reporting is accurate and transparent.

Efficient Document Management:

We assist you in organizing and streamlining your financial documents, making it easier to compile the necessary records for an FTA audit.

Pre-Audit Assessments:

Our pre-audit services help identify potential issues well before the official audit, allowing you to rectify them and reduce the risk of non-compliance.

3. Transparent Reporting and Clear Communication

Comprehensive Audit Reports:

We provide detailed, easy-to-understand reports that break down complex financial data into actionable insights.

Ongoing Communication:

Our team maintains continuous dialogue throughout the audit process, ensuring that you are informed at every stage and can address any issues promptly.

Actionable Recommendations:

Our reports include practical recommendations to enhance your internal controls, optimize tax efficiency, and support continuous improvement in your financial management practices.

4. Ongoing Support and Long-Term Partnership

Post-Audit Assistance:

Our commitment to your success extends beyond the audit report. We offer ongoing support to help you implement our recommendations and monitor your financial performance.

Continuous Monitoring:

We set up systems for regular financial monitoring to detect and address potential issues before they escalate.

Client-Centric Partnership:

At Young and Right, we view our relationship with you as a long-term partnership dedicated to your ongoing growth and financial health.

Conclusion

Failing a tax audit can result in severe legal and financial consequences, from hefty fines and increased tax liabilities to legal action and operational disruptions. However, with diligent preparation, robust record-keeping, and proactive risk management, businesses can significantly reduce the risk of audit failure and its associated penalties.

By maintaining accurate financial records, enhancing internal controls, and engaging in regular pre-audit assessments, you can build a strong foundation for tax compliance. In addition, fostering open communication and investing in professional guidance are key to ensuring a smooth and successful audit process.

For businesses in the UAE looking to navigate tax audits with confidence, partnering with experienced professionals like Young and Right is crucial. Our expert analysis, tailored preparation strategies, transparent reporting, and ongoing support empower you to address any potential issues before they escalate into significant problems. Embrace proactive tax management and secure your company’s financial future with the trusted guidance of Young and Right.